Did you know?

ChinaBio® Group is a consulting and advisory firm helping life science companies and investors achieve success in China. ChinaBio works with U.S., European and APAC companies and investors seeking partnerships, acquisitions, novel technologies and funding in China.

Free Newsletter

Have the latest stories on China's life science industry delivered to your inbox daily or weekly - free!

Free Report

The State of China Life Science – IPOs and M&A

Introduction

Because of the worldwide financial downturn, business activity is shrinking almost universally, though some individual areas are demonstrating relative strength – and we think the life science industry in China is one of those areas. In this series of articles, ChinaBio® presents proprietary data developed by its own team of researchers that explains why we remain cautiously optimistic about China life science.

In earlier articles, we first presented an overview of the current state of China life science (see story), then original research on the life science patents that have been filed in China since 2000 (see story), and next the venture capital investments in life science during 2008 (see story). Here, in the concluding part of the series, we discuss recent deals in the sector, including IPOs and M&A.

IPOs are Dead

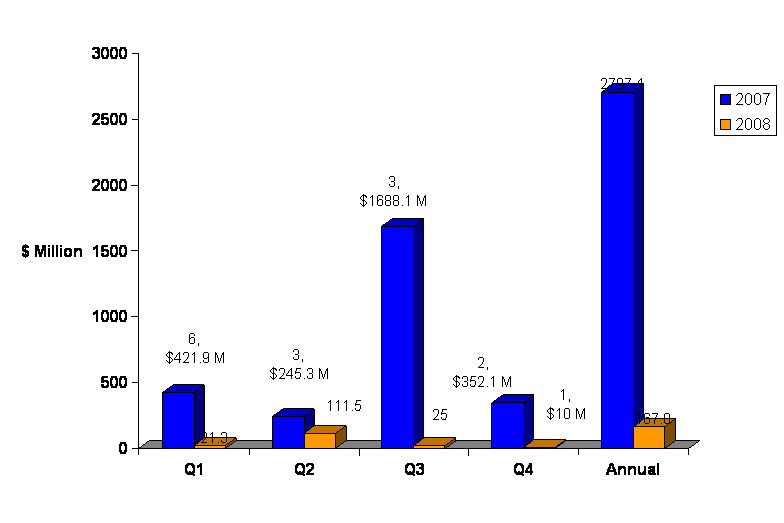

Affected by the global financial downturn, the IPO is no longer available as an exit for VC or PE investors. In 2008, only 5 China life science companies went public, raising $167.8 million, an average of $33.6 million for each IPO. That was a 94% decline from 2007, when 14 companies raised $2,707.4 million, representing an average of $193.4 million per IPO. Because of the current state of economic uncertainty, IPO activity will remain depressed until the financial crisis is resolved. However, some companies, such as CP-Guojian and MicroPort Medical (Shanghai), are preparing to go public when the IPO window reopens.

Figure 1 – 2007/2008 IPO Activity

By Stock Exchange

In 2007, ten China biopharmaceutical companies (71% of the total) went public in stock exchanges outside of mainland China, while four listed on the Shenzhen exchange. Among the ten biopharmaceutical companies that went public overseas (including Hong Kong), five were backed by VC or PE investments.

In 2008, the numbers were much smaller. Just four biopharmaceutical companies listed on the Shenzhen exchange and one in Hong Kong. There were no NYSE, NASDAQ, AIM, SGXM or other overseas stock exchange IPOs. And only one, Jiangsu Yuyue Medical Equipment & Supply, was backed by a VC firm (ShenZhen ShiFangLian Venture Capital), which exited in the IPO. This means the window of overseas IPOs is firmly closed, much like that for domestic stock exchanges. XBy Industry

In 2008, only companies in Traditional Chinese Medicine, medical devices and generic biotech industries went public, a smaller cross-section of the life sciences industry than in 2007, which also included service companies and distributors. Because VC or PE backed companies prefer an IPO as an exit path, IPOs remain scheduled in the future for some of these companies. Considering the number of companies that received VC or PE investments in the last few years, especially those in late stage, there may be an upsurge in IPOs when the IPO window reopens. (See State of China Biotech – VC Investment)

M&A Still Active

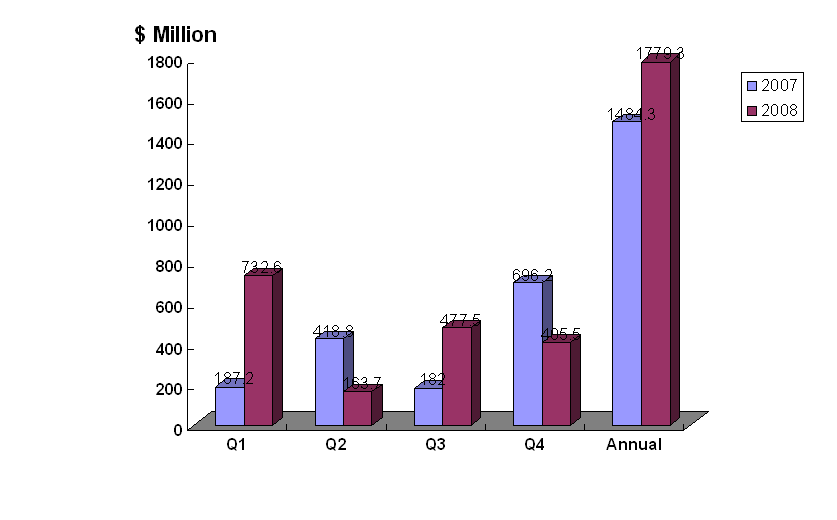

In 2008, there were 61 M&A deals (33 with disclosed amounts) in China biopharma representing a total value of $1.77 billion. That surpassed the 2007 results, despite 2008’s financial crisis. In 2007, 33 deals (24 with disclosed amounts) were completed with a dollar value of $1.48 billion. That means more transactions and a higher total value took place in 2008, though the average deal size dropped from $61.8 million in 2007 to $53.9 million in 2008.

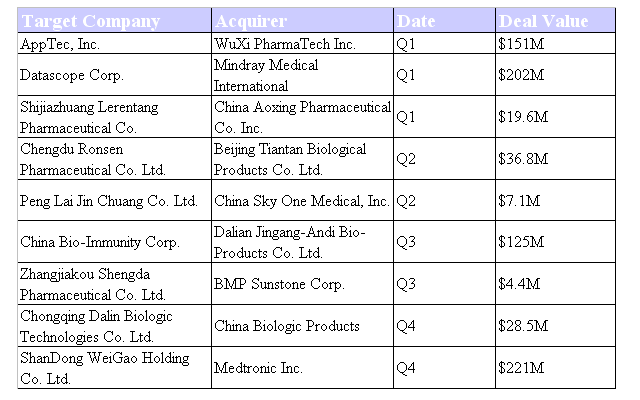

However, 2008’s higher total was helped by a strong Q1 – before the economic problems were manifest. The biggest percentage of the action took place in Q1 of 2008, with a significant falloff as the economic crisis spread around the globe. Eleven deals with a value of $732.6 million were announced in the first quarter – that's 41% of the dollar total, though it was generated by one-third of the number of transactions. During Q1, there were several large transactions. Most notably, WuXi PharmaTech (NYSE: WX) bought AppTec for $151 million, and Mindray Medical (NYSE: MR) paid $202 million for Datascope's (NSDQ: DSCP) patient monitoring business.

PricewaterhouseCoopers noticed a similar trend across the entire spectrum of China M&A activity. According to the firm's research division, the first half of 2008 saw an increase of activity. The 543 deals announced in the first six months were up 14% over the year-earlier numbers. On the other hand, in the second half, up to November, the number of announced transactions dropped 47% from 2007. XPWC expects the slowdown to continue through the first half of 2009. Then, when the confusion caused by the economic crisis has settled down, buyers and sellers will be more likely to agree on valuations, and activity will pick up, in the company's forecast.

For China biopharma, the slowdown was already evident in Q2 of 2008. Total deal value dropped 77% from $732 million in Q1 to $163 million in the second quarter. The action picked up from there, as $477 million of M&A activity was done in Q3 and $405 million in Q4. The Q3 total received a big boost from the $125 million deal in which Dalian Jingang-Andi Bio-Products Co. Ltd. acquired China Bio-Immunity Corp. (See Table 1)

Figure 2 -- M&A by Quarters in 2007 & 2008

Table 1 – Sample 2008 M&A Activity in China Life Sciences

By Industry

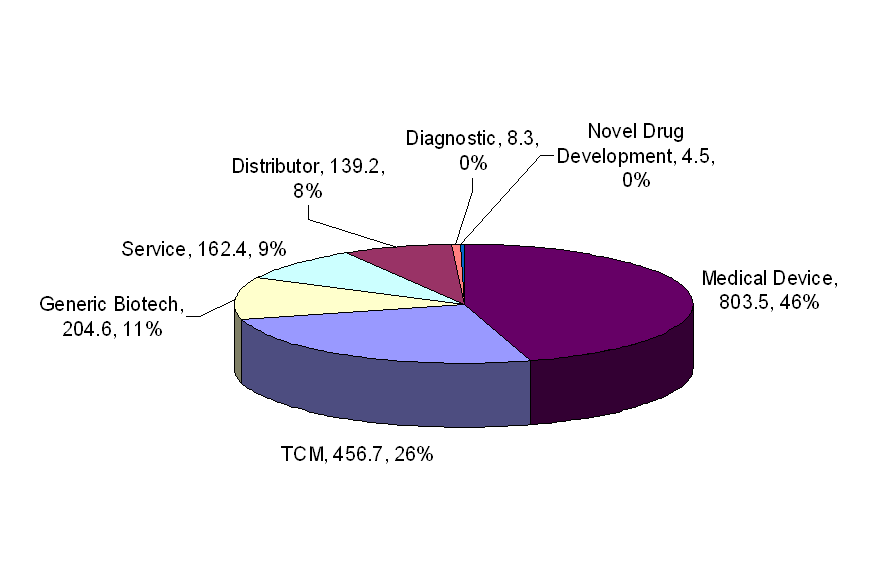

In 2008, a major shift took place, diminishing the importance of TCM companies. In 2007, traditional Chinese medicine companies represented 74% of the total M&A dollars ($1084.1 million), but that dropped to just 26% in 2008 ($456.7 million). Medical device companies, on the other hand, jumped from a meager 3% of the 2007 pie ($50.1 million) to a much larger 46% of the ten-month 2008 numbers ($803.5 million). The M&A in generic biotech and service sector increased to $204.6 million and $162 million respectively in 2008. However, M&A involving novel drug development companies was relatively low compared to that in 2007.

Figure 3 – 2008 M&A Activity by Life Science Specialty

Other 2008 M&A Facts

Most of the 2008 deals were done between companies in the same industry: 85% (52/61) of the total last year compared to 75% (24/32) in 2007. In 2008, only nine deals were closed between companies in different industries, usually distributors and novel drug development companies that were acquired by medical device companies, traditional Chinese medicines or traditional biotech companies. For example, Biosensors International acquired 80% of JW Medical Systems in a step-by-step process; the latter was the distributor of the former.

M&A between Chinese pharmaceutical companies and MNCs or foreign companies increased to 27 deals in 2008 from 4 deals in 2007. Among the multinational mergers, two MNCs acquired their JV subsidiaries by purchasing the shares held by a Chinese partner; one was a reverse merger. There were five M&A transactions in the service field, all of which were between local companies and foreign companies. XAmong multinational M&As, some of the deals are very well known. For example, Wuxi PharmaTech acquired US AppTec; Frontage Laboratories acquired Advanced Biomedical Research (ABR); Venturepharm Laboratories acquired Commonwealth Biotechnologies; Mindray Medical acquired Datascope and so on.

After reviewing the mergers in our database, we find that companies with money in their pockets are very likely to do M&A, especially in a time of financial crisis when prices are lower than usual. The cash-rich companies include leaders in the industry with good revenues or companies that raised money from IPOs or VC/PE investors.

Trend

Because M&A is a money-based activity, the financial crisis of 2008 has closed the IPO window and made VC and PE investors more cautious. A lower level of M&A activity will continue in 2009 (and perhaps longer) until conditions improve. But when M&A activity begins to rise again, medical device and traditional Chinese medicine industries will probably re-emerge as leaders. As in 2008, MNCs will be still a major force for M&A. China’s life science industry remains highly fragmented, so consolidation can be expected, and domestic companies will also take advantage of M&A to increase their revenues and profits.

Disclosure: none.

ChinaBio® News

Greg Scott Interviewed at BIO-Europe Spring

How to bring your China assets to China in 8 minutes

"Mr. Bio in China."

Mendelspod Interview

Multinational pharma held to a higher standard in China